Global Listed Infrastructure September 2021 Monthly Commentary

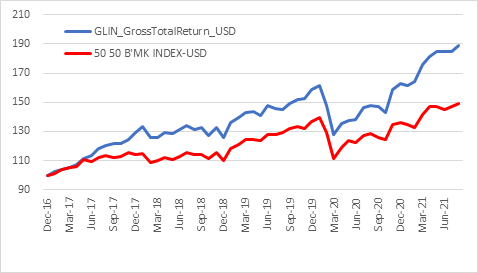

Global markets have once again conformed to the market anomaly of the September Effect. A modest correction was felt in all major markets with the S&P500 down 4%, Euro Stoxx also down 4% and the Hang Seng down 5.5%. The AOP Global Infrastructure Index strategy returned -2.6 % in A$ for the month of September outperforming the benchmark by 0.5%.

In the US, Congressional horse trading has continued surrounding the Infrastructure Bills. Arizona Sen. Kyrsten Sinema and West Virginia Sen. Joe Manchin are proving to be the sticking points for the Biden administration’s much needed infrastructure spend. The Democratic senators should note that the American Society of Civil Engineers graded the crumbling infrastructure in Arizona as C and West Virginia as D in the 2020 infrastructure report.

It seems the Senate has voted to kick the debt ceiling can down the road which should relieve some short-term pressures on markets, however this will remain a significant risk factor over the next months.

Inflation pressures continue to rise as disruptions to global supply chains continue to play havoc. The strategy has maintained an overweight exposure to the logistics and transportation industries during these disruptions but began taking profits in this sector in the 3rd quarter.

The inflation rhetoric now seems to have shifted from the transitory to enduring. Despite recent posturing from the Federal Reserve, we believe the prospect of shifting from the current low interest rate environment to substantial and sustained interest rate increases are unlikely given current economic conditions. While many similarities superficially exist between the 1970s stagflation and today, there is a meaningful and critical difference which is the relative power of Labour vs Capital. Consequently, we see no need for large increases in interest rates to pressure companies to lay off employees and generally dampen wage inflation. We do see regulation to reduce the power of monopolies and monopsonies and coercion of companies to raise wages. This should be a tailwind to inflation but also act as a restraint on corporate profit margins. eg the Surface Transportation Board was asked by the Biden administration to assess the lack of competition in the railroad industry. This increased regulation is a risk globally to all companies including infrastructure.

Chinese markets to continued show volatility in September as regulatory risks regarding restructuring efforts in the economy remain. Regulatory risks are not confined to China. The Spanish government hinted at revisiting the prices for wind sourced electricity which has shot up in price in sympathy with gas prices. This hurt the share prices of Iberdrola and ENEL in Italy. These are difficult risks to predict but our guess is that the fiscally strapped European governments will be the most tempted.

Energy prices rose dramatically for several reasons and renewables are not (yet?) capable of meeting spikes in demand. Given the zeitgeist demanding ’Green’ energy and the German push to get Nord Stream 2 online we believe that gas will be seen as a clean energy (or at least a less dirty option) for at least the near future.

Enbridge line 3 replacement has now started flowing despite substantial protests in various US States. Enbridge line 5 remains a political football in Michigan with Canada formally invoking article 6 of the 1977 transit pipelines treaty which will force the Biden administration to take part in the line 5 dispute. We favour gas utilities and pipelines for utility exposure the index added small positions in NRG, Org Energy, Entergy and WEC Energy as we look to diversify in the sector.

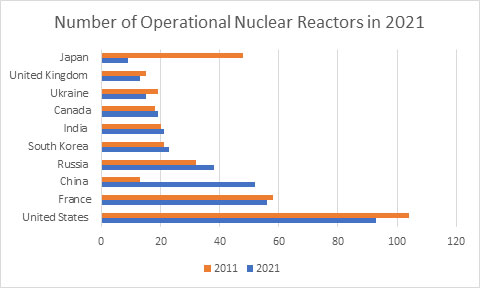

We also note the increasing news flow regarding nuclear power and fully expect that to be floated as a clean energy – which it is. The chart below shows the existing state of the global nuclear power generating industry, and those countries growing and those shrinking the nuclear reactor count.

Net zero would seem to be a difficult task without a substantial investment in the forgotten carbon free baseload power generation of nuclear power. We expect to see public sentiment and in turn, political will to shift in relation to nuclear power. New Japanese Prime Minister Fumio Kishida has already hinted at restarting the country’s nuclear power plants (presumably after seeing Japan’s Nat Gas bills) the majority of which have remained dormant since the 2011 Fukushima meltdown. Post Fukushima it has been the stance of the Japanese Government to no longer refurbish or construct Nuclear Plants (we expect this to change). Ageing US Nuclear plants will also see a new lease of life after the Illinois state senate approved a US$700m subsidy to Exelon to keep the Byron and Dresden plants open. Moreover, NextEra Energy has asked the Nuclear Regulatory Commission to extend the licenses for two rectors at its St Lucie Plant for a further 20 years after already receiving approval to extend the life of its Turkey Point Plant for 20 years. Should approvals at St Lucie be granted the life of these plants will have been 80 years (yes 80!) when they are finally taken offline. Whilst modern nuclear plants offer a safe and clean (mostly) source of baseload power a lack of investment in new plants in the majority of developed nations has resulted in ageing plant extending their lives despite the numerous risks attached. 57 nuclear plants are under construction globally with bulk of this construction occurring in Asia. The US and UK both have 2 plants under construction with an average age of plants of 39 and 36 years respectively and we expect this number will need to increase in the coming years. The index maintains exposure to nuclear power generations through diversified electric utilities.

The approaching Northern Hemisphere winter will keep upward pressure on energy prices. If we were asked, we would recommend that a switch to Carbon Neutral be only done when sustainable energy technology can provide base and peak load power. Currently it is not. As such continued investment in traditional but cleaner than coal energy sources would make sense.

Notable performers in the index for the month were Chinese wind producer China Longyuan Power rising 21.3% and Natural Gas Utility ONEOK rising 11.3%.

The index is currently overweight Transportation and Logistics despite recent profit taking and still substantially underweight integrated telecommunications. Active risk levels to the benchmark have been reduced to an average of 4%.