Nextera Energy – Growth and Yield? Or “Having your Cake and Eating it”?

17th September, 2020 - Delft Partners

Infrastructure companies are essential providers of facilities and structures for the effective operation of a business, state, or economy. They are indispensable to sustainable growth and enjoy stable demand, growing profitability and provide above average yields to equity investors.

Listed infrastructure companies are currently very attractive investments. Many pay high sustainable dividends and their revenue streams are consistent and secure. Our estimate of the Beta of the infrastructure universe is 0.8 relative to the broader global equity universe. This means that the listed equity infrastructure category will not fall, nor rise as much as the general market. At a time when government bond yields have been suppressed to virtually zero and when equity market volatility is likely to rise, this means that the listed infrastructure 'asset class' offers yield and safety. Something which used to be the role of bonds, but which now appears to be beyond them?

We have termed the global infrastructure opportunity as one defined by:-

Renovation – the need to move infrastructure from 3rd World to 1st World status in the USA and much of Europe

Reinvigoration – expanding infrastructure will raise productivity and provide a fiscal multiplier boosting sustainable economic growth

Restitution – the adoption of cleaner renewable and recyclable will raise the quality of economic output.

This is a brief article on a company which fulfils all 3 criteria. It is a core holding in our Global Infrastructure strategy.

Electric utilities are key infrastructure companies, and while not the most exciting of companies to read or write about, it is often the case that boring companies can be great investments.

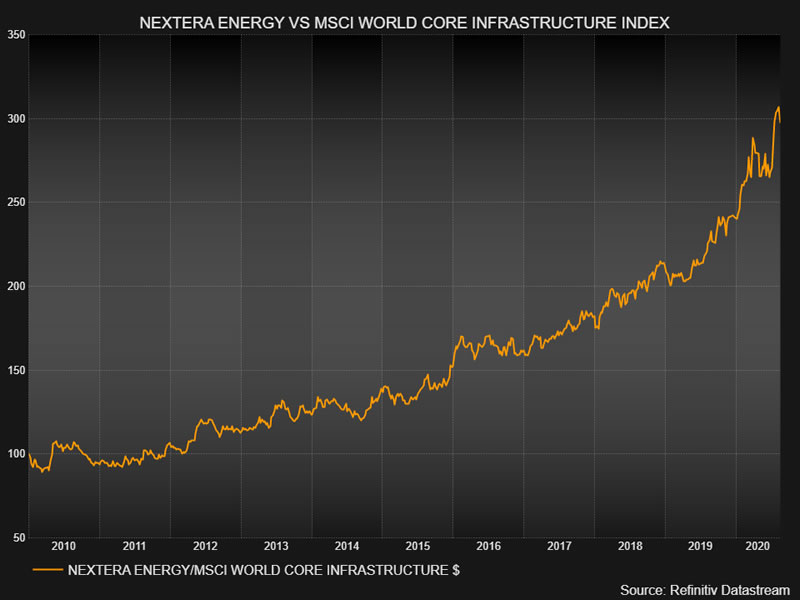

Nextera Energy (NEE) in the USA has been a great investment despite just being an electricity producer, but it is interesting how it actually achieved this because it may help us to find the next "Nexteras".

It is now the largest utility company in the world by market value and the largest producer of wind and solar energy in the world. It has certainly done well for its shareholders. Over 15 years its annualised earnings growth has been 8.4% and its dividend growth has been 9.4%. But even more impressive has been its share price rising 10x over 15 years at an annualised rate of 17%!

Given its good operational performance of earnings and dividend growth it has certainly been well managed with judicious use of capital and M&A activity. It has also played in to 2 key themes.

- It has significantly increased the proportion of its electrical production from renewables – wind and solar power - and

- has also significantly increased its battery storage technology and capacity. So, it now has the largest battery storage capacity in the world.

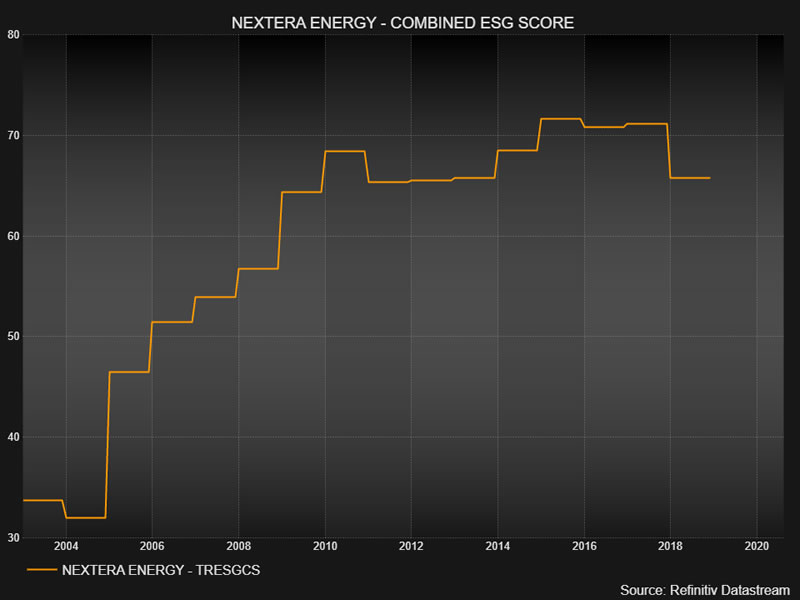

These have played well with institutional investors that have been under pressure to invest in a more environmentally conscious way.

A cynic may say that it has also been very good at marketing itself too and communicating all the right messages to the investment community. You won’t find much mention of the fact that it still has some of those nasty carbon burning power plants in its investor presentations!

Nextera has also explicitly targeted raising its ESG (Environmental, Social, and Governance) scores in other aspects. So Nextera has been ticking a lot of the boxes for investors. As a result, Nextera now trades at a significant valuation premium to other electric utilities at 30x PE for 2021. So, while it is likely that its best returns for shareholders are behind it but it could yet still outperform its peers; and provide a stable source of income and capital return in a world where government bond yields have been suppressed to virtually nothing.

As we move increasingly to electric vehicles (EVs) then this is likely to be a significant boost for electric producers and lead to significantly better growth prospects. So, it should become a more attractive sector with rising valuations, and we should see more M&A activity particularly in more fragmented markets like the USA. So, it’s a sector we prefer within the Global Infrastructure universe right now, with good earnings and dividend visibility in this Covid-19 economic environment.

Many countries are likely to run in to electrical capacity constraints – indeed lots of emerging economies already have capacity issues. As countries decommission oil, gas and nuclear plants so there will be a significant demand for wind turbines, solar panels, hydro electric turbines and other capital goods related to the electrical power generation industry.

We are in the middle of a low carbon industrial revolution as companies commit themselves to lowering their carbon footprint. Although Covid may curtail some companies from spending money on capex to be more environmentally friendly it is unlikely to be the electrical producers where project times are long, and they usually have regulatory commitments. Key beneficiaries from project work like this would be Schneider Electric, Mitsubishi Electric, Siemens, GE, Honeywell, ABB and Vestas Wind Systems. We will write about these in the months ahead.