April 2026 Update

April, 2026

March Madness?

Not the NCAA but another Middle East 'adventure' which creates perhaps more problems than it solves? Oil and other commodities rose strongly in March, and the extended equity markets saw the perfect excuse to sell-off. Is this worse than the first and second oil shocks of the 1970s? No. Does this show the vulnerability of economies which have failed to secure energy security and the importance of uninterrupted and affordability of oil and gas? Yes. European 'think' tanks and even politicians are beginning to walk back on the “All Renewables” policy. Europe is now buying Russian gas, has promised Euro billions in support to the Ukraine, and thus appears to be paying Peter and Paul and robbing itself.

Our central case remains that a structural dash for energy and material security and a re-industrialisation will drive a re-appraisal of the very stocks which have been out of favour for many years. Add in the balance sheet constraints (and increasingly obvious creative accounting?) of the tech darlings such as Meta and Oracle and the 'maximum pain to the maximum number of investors' role of the market will have been again realised. We have pointed out that with $1 trillion of buybacks supporting share prices, particularly of the heavily favoured stocks, but now a promised surge in capital investment, that the “free” cashflow of many of these largest companies will become er …'constrained'. If buybacks cease, then share market support is removed. If capital investment fails to meet promises, then analysts will question the growth rate and there will be downstream implications for the A.I. ecosystem. No surprise then that head count is being rapidly and massively reduced in many companies? Way back we did use headcount changes in a quantitative model as indicative of management confidence in their companies' prospects. Time to revisit?

As per the last few commentaries we have been positioned for realisation of the value of HALO companies and so outperformed handily this quarter.

https://www.delftpartners.com/news/views/march-2026-market-commentary.html

https://www.delftpartners.com/news/views/february-2026-remember-newtons-third-law-of-motion.html

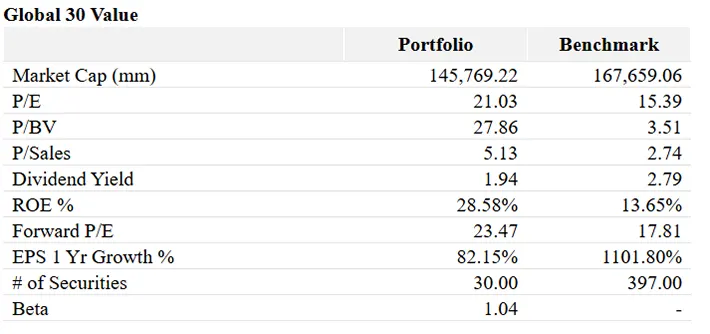

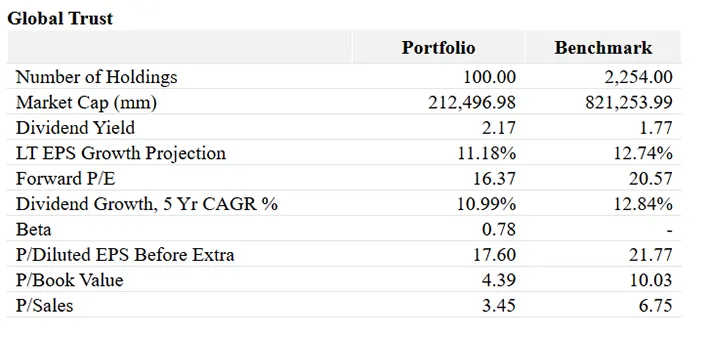

The Global Trust, a diversified and risk managed global equity strategy rose c. 6% gross of fees in the first quarter, ahead of its benchmark by about 13% and over the last 3 years c22%, ahead of the benchmark by c.5% p.a. The Global 30, a Value biased strategy drawn from stocks in the Global Trust, rose c.5% in the quarter and c.22% in the last 3 years to end March, ahead of its Value benchmark by c.5% p.a. Having traded heavily at end February to reduce Momentum exposure we did little in March apart from take profits on some oil stocks such as CNOOC and Inpex.

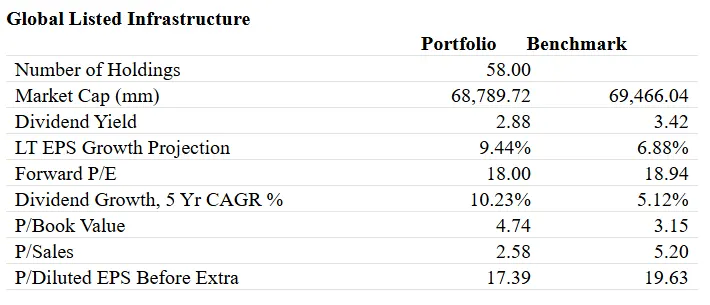

Global Listed Infrastructure also performed well in the quarter, rising c.7%. We made quite a few trades in this strategy during March - selling or reducing NTT, Veolia and China Merchants and buying or adding to BW LPG, Terna, and Entergy.

We have ceased to produce quarterly fact sheets since all that information can be readily accessed elsewhere. As a summary of current portfolio characteristics, we present the March end summary in tables below.

Our Momentum risk exposure remains very elevated due to sheer outperformance. Many stocks, relative to others look stretched on price momentum and valuation. At some point we may take a deep breath and invest more heavily in banks. We'd just like to see a serious clear out of the private credit (and equity) carrying values.

Sell in May and go away?

Delft Partners April 2026

DISCLAIMER

This report provides general information only and does not take into account the investment

objectives, financial circumstances or needs of any person. To the maximum extent permitted by law,

Delft Partners Pty Ltd, its directors and employees accept no liability for any loss or damage

incurred as a result of any action taken or not taken on the basis of the information contained in

the report or any omissions or errors within it. It is advisable that you obtain professional

independent financial, legal and taxation advice before making any financial investment decision.

Delft Partners Pty Ltd does not guarantee the repayment of capital, the payment of income, or the

performance of its investments. Delft Partners operates as owner of API Capital Advisory Pty Ltd

AFSL 329133.