Is China ‘Un-investable’?

September 2021

By Delft Partners

Investing in China remains a moral question but to not invest now because of more government intervention and capricious legislation, is illogical since that would be to ignore the fact that the trends toward more government intervention and legislation are evident in other countries. More government, capricious and unexpected legislation to the apparent detriment of companies and shareholders, is now omnipresent as a global systemic risk to equity returns. Consequently, prepare for lower rates of profit growth and ‘fatter’ tails in your investment outcomes, even if you decide to never invest in China again.

There are similarities between Xi Jinping's increasing intervention in the Chinese corporate sector and those by Western governments.

- Policy with social objectives (with a lack of awareness or acknowledgement that years of free money created the wealth inequality in the first place)

- More taxation and worryingly more centrally directed capital allocation and subsidies (Tesla anyone?)

- Penalising ‘rentier capital’ aka private savings

- Coercion of the population to behave by scare tactics/messaging, and surveillance. China uses facial recognition software and uses ‘social scores, but you may care to read this? https://www.amnesty.org/en/latest/news/2021/06/scale-new-york-police-facial-recognition-revealed/

At least China has finally done something about moral hazard which would still seem to be prevalent in ‘the West’? China Evergrande is 95% certain to default on over $100bn of debt including bonds, and we’ll have to see how that pain gets allocated between locals and foreigners before making more judgements, but bankruptcy is part of capitalism, or it used to be. In this respect China is ahead of the US perhaps and certainly the Europeans in letting a failed enterprise actually fail to the detriment of investors rather than the general tax payer.

For those of you who think that China’s decision making comes without due warning and therefore makes it too risky a market in which to invest, the second part of the US ‘Infrastructure’ bill equal to a 3.5tln $ spend, will take all of 17! days to debate.

Obamacare took 9 months even with a significant Democrat majority, (which is not the case now) and FDR’s programmes were spread over his first 2 terms – 8 years. The UK government recently announced hikes on national insurance and dividend tax increases in essentially a unilateral decision by the prime minister. The unelected European Central Bank has essentially decided both monetary and fiscal policy for Europe and the result has been less than stellar growth. The Euro remains a political construct not a valid economic one but it’s an ideology akin to ‘Mao thought’ and so on we go regardless of contravening evidence from what remains of the ‘free market’.

In short, governments and their agencies everywhere are consulting less and intervening more and more quickly.

Government exists to provide essential services but to also redress other imbalances dangerous to national cohesion – or they should. Currently imbalances are very evident in wealth inequality and the share of profits in the economy relative to wages.

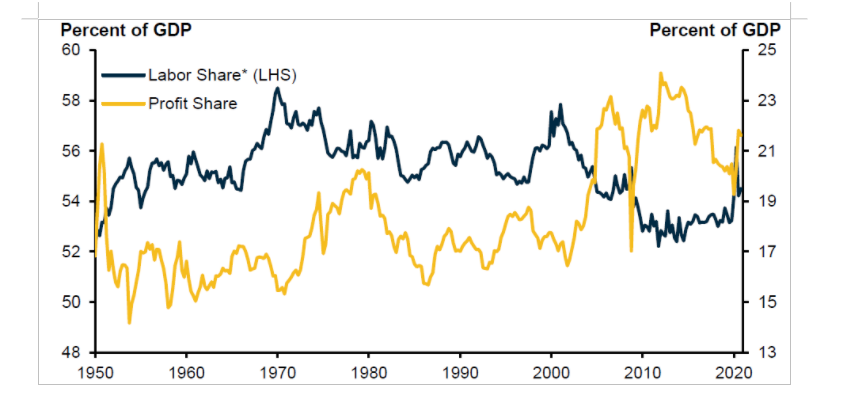

Using the US data (the best around) we can see from the chart below, that corporate profits have been on a rising trend relative to wages. Since the consumers of the companies’ products need money with which to buy them, this % allocation tends to oscillate around an average. If wages rise too quickly then companies become less profitable, can’t invest, and won’t hire which then reduces wage growth. Vice versa. Sometimes a nudge, or more, is needed – the General Strikes in the 1920s, the Reagan, Thatcher, Laffer curve revolution of the late 1970s and the Schroeder reforms in Germany in the 1990s serve as examples.

This swing back to relative growth in wages is needed and will introduce bigger government as the source of the nudge. Don't blame government - blame companies that have indulged in such crappy anti-social behaviour as zero contract hours, and paying no taxes while enjoying the legal protection, trained workforce, and infrastructure that other people's taxes have provided. This government intervention could have been prevented in the last few years had companies perhaps not bought back stock to the tune of c$900bn p.a. significantly benefitting corporate executive share option schemes, and instead raised wages, increased re-investment and improved job security? This imbalance also got a big tailwind from ZIRP aka “monetary policy for rich people”, and so governments are also culpable in running with ZIRP for too long. However, don’t expect them to take a hit or apologise. ESG activism has a role perhaps, but we don’t see that level of nuance from shareholders - yet?

Investors should view this shift as an essential rebalance, because without we would be heading for a worse outcome – capital controls, confiscation of property and financial repression all await and have been implemented before.

Economic distress causes revolutions and if you want examples throughout history checkout this book by David Hackett Fischer.https://en.wikipedia.org/wiki/The_Great_Wave_(book)

Two final thoughts:

- Trickle-down economics is dead and as investors you should prepare for more government; National Industrial Polices, thus more inflation and taxation; and thus, lower returns from equities. Our advice is focus on smaller companies since they are seldom directly in the firing line of legislation; find companies that do ‘useful things’ such as building a country’s capital stock; look very closely at Japan which we think both cheap and showing change for the good, and arguably has less inequality to correct; and increase the volatility of expected returns if you do such things as portfolio optimisations, trading off risk and return.

- The moral issue of investing in China requires consistency? – if you don’t like the idea of benefitting from profits made in China’s repressive regime, shouldn’t that ‘dislike’ encompass the rejection as unacceptable, of any profits made in China, regardless of the geographical listing and domicile of the company?

By Delft Partners

September 2021