A review of H1 2022 - We are at a crossroads. July 2022

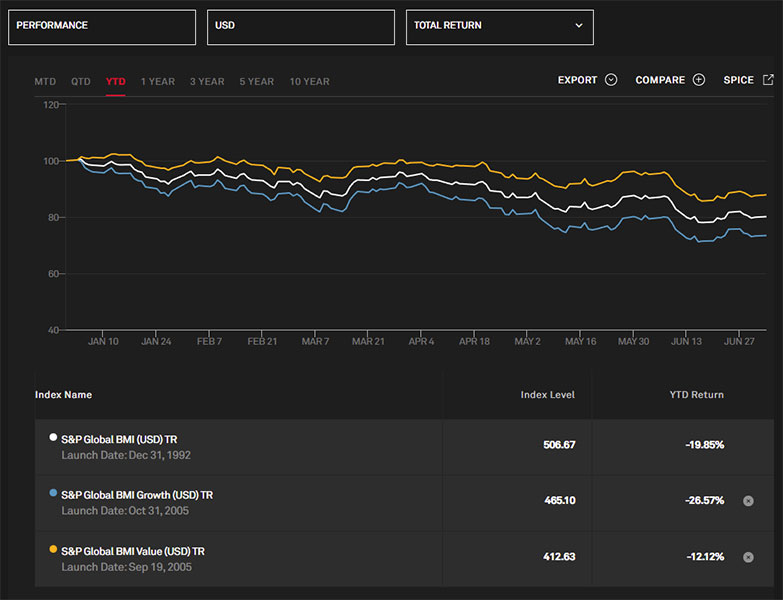

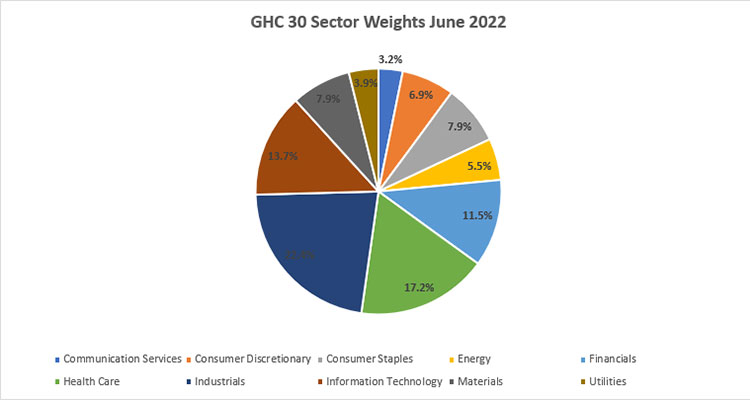

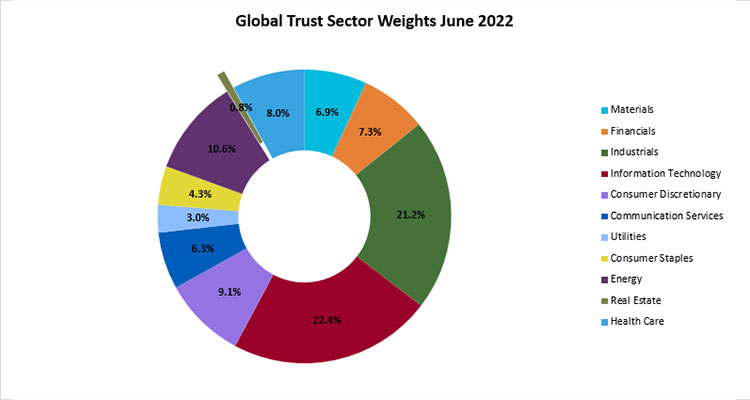

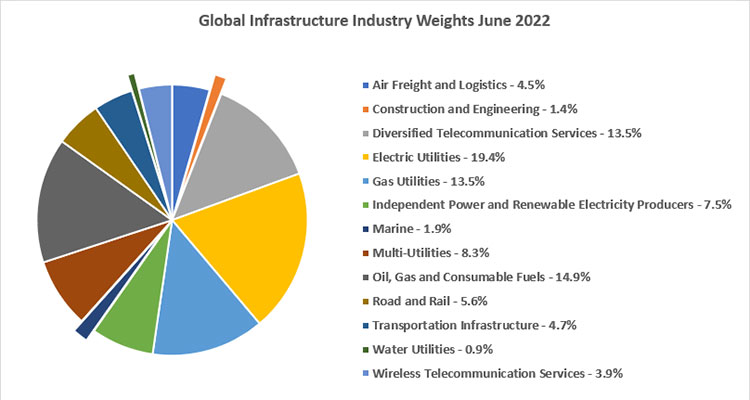

The end of June was maybe a relief, for it was a tumultuous quarter and half year of negative returns for most asset classes. Global equities, as measured by the S&P Global BMI, posted their worst first half performance since index inception, and with a decrease of 8.5% in June, were down 20.4% in H1 in US$. The A$ decline mitigated the fall somewhat. In June, the Global Equity Trust a diversified strategy benchmarked to the capitalisation weighted indices fell 5.7% in A$ and the GHC 30, a more value biased portfolio of 30 stocks derived from the trust holdings, fell 3.6%. The Global listed infrastructure declined 2.4%. Year to date, -12.2%; -8.8% and -2.3% respectively.

Equities - a bad month quarter and half-year

Fear has truly gripped the equity markets with losses accelerating significantly in the just-concluded quarter. Global equities returned -14.3% in the quarter, accounting for almost 80% of the total losses year-to-date. In USD terms losses have been quite similar across the world save for the UK where the heavy weighting of oil stocks saved the market from serious losses. The dollar's strength though has only exacerbated losses for dollar-based investors. The Japanese equity markets is a good case in point - in JPY terms, it was only down 5.9%, but the slump was more drastic - 20.3% - in USD terms. The UK was up 1.7% in local currency terms. The energy sector was the only major sector to record gains in the first half of the year, managing to shake off most of the losses seen in the broader markets. However, as the quarter ended investors got anxious that the risk of recession could lead to challenges for oil companies, irrespective of the fact that the market remains in marked short supply.

Major Equity Markets-losses accelerated in the second quarter

| Total Returns | 1H | Q2 | ||

|---|---|---|---|---|

| Local | USD | Local | USD | |

| MSCI World | -20.5% | -18.3% | -16.2% | -14.3% |

| MSCI US | -21.3% | -21.3% | -16.9% | -16.9% |

| MSCI Europe ex UK | -11.9% | -20.8% | -8.1% | -14.5% |

| MSCI Japan | -5.9% | -20.3% | -4.4% | -14.6% |

| MSCI UK | +1.7% | -8.8% | -2.9% | -10.5% |

| MSCI Asia Ex Japan | -11.6% | -16.3% | -6.9% | -9.0% |

| Emerging Markets | -13.7% | -17.6% | -8.1% | -11.4% |

| Sectors | 1H | Q2 |

|---|---|---|

| Energy | +24.0% | -5.1% |

| Consumer Discretionary | -31.9% | -23.8% |

| Banks | -18.6% | -16.2% |

| Tech | -29.7% | -21.8% |

Source: Bloomberg

Not many places to hide

Bonds didn't do their job - Global Bond returns for the first half of 2022

| Total returns | 1H | Q2 |

|---|---|---|

| Global Aggregate | -9.1% | -4.3% |

| US Aggregate | -10.3% | -4.7% |

| Global High Yield | -15.2% | -10.6% |

| China Aggregate | -3.1% | -4.3% |

bps change

| US 10-year bond yield | 150 | 68 |

| US 2-year bond yield | 144 | 62 |

Source: Bloomberg

We continue to believe that the world is facing a structural shift in risks. It is no longer the case that "well-behaved" inflation will allow central banks to provide virtually free liquidity to pump up asset prices. The end of (and failure of) the era of ultra-cheap money and the put option will mean that many companies and bonds will not be around when the strain of higher interest rates and lower revenues begins to bite. One could argue that in this regard the era of free money has seen developed economies turned into emerging market economies - we now have unsustainable debt, inflation, currency debasement and default, wider inequality, poorer quality government services and more corruption?

All characteristics of "developing" economies and not of developed?

A brief review of the first half economic backdrop

In the first half the key change in sentiment amongst economists and central bankers has been the marked deterioration in their outlook for inflation. Inflation has continued to significantly surprise to the upside through the first half of 2022. Interestingly though forecasters have been late in pressing the warning button about their outlook for inflation. Inflationary pressures have actually been building up over the years of central bank balance sheet expansion. Once the supply side became too strained (Covid shutdown, energy transition and re-onshoring) and demand became pumped up (Fiscal handouts) there was an inevitability. The problem is that the supply side, other than labour, will take a long time to (re) build.

True to form the experts' growth forecasts have only just recently started turning negative. There will be further downgrades. Group think, academic arrogance, and an addiction to outmoded models are a toxic mix.

Update On Central Bank Failures In Inflation Management

We couldn't resist to remind you of these rebuttals of the dangers of inflation with (sort of) apologies to the authors:-

- "There's nothing to suggest a recession is in the works" - Janet Yellen, last week

- "I wouldn't do it differently. I was very supportive of the American Rescue Plan." - Janet Yellen, last week

- U.S. inflation risk is "small" and "manageable" - Janet Yellen, March 2021

- "I don't anticipate that inflation is going to be a problem" - Janet Yellen, May 2021

- "In the 1970s, a series of supply shocks became a longer run problem ... that partly occurred because policy makers weren't trusted by the public to deal effectively with inflation. But I certainly see no evidence that that's the case now." - Janet Yellen, November 2021

- The Fed "shouldn't overreact to 'temporary' inflation" - Neel Kashkari, November 2021

- "There's nothing that I'm seeing in these fundamental factors that leads me to think that this is a long-term change in inflation or inflation expectations." - Neel Kashkari, November 2021

- "If we overreact by saying 'let's change the path of monetary policy'…that could lead to a worse long-term outcome for the economy."- Neel Kashkari, November 2021

- "What's the economic theory that a one time boost of fiscal spending, a one time boost of demand - it leads to higher prices, yes - does it lead to higher inflation, which means ongoing year after year after year of continuing price increases. I don't really understand the mechanism by which Larry Summers thinks this one time fiscal stimulus leads a change in the path of inflation." - Neel Kashkari, November 2021

- "The key here is from my perspective as a Central Banker is not to overreact. We want to pay attention to the data, we want to look at the evidence and we want to make our adjustments prudently, not just overreact because Twitter is hyperventilating." - Neel Kashkari, November 2021

- "I can't predict the future any better than Bill Dudley can." - Neel Kashkari, November 2021

- "Inflation is higher than I expected, and it's the high inflation has lasted longer than I expected. We know the US economy is recovering from the COVID shutdown and the downturn. But the recovery is uneven, and demand has recovered more quickly than supply has. So given those facts, it's not that surprising that inflation is coming up higher than we expected. But it should start to normalize over the course of this year, if a couple things happen: if workers come back into the job market. We're still missing 3 or 4 million workers. And if supply chains start to sort themselves out, which I hope that they will. But obviously the Federal Reserve has an important role to play and we're going to do our part." - Neel Kashkari, January 2022

- "So that's why the fact that the yield curve has flattened a lot over the past six months, that's giving me some indication that we're probably not that far away from neutral, not as far away as maybe we thought." - Neel Kashkari, January 2022

- "So, you know, neutral is a concept and so it's not as if there's an equation exactly where it is. For me, it's somewhere between 2 and 2.5 percent." - Raphael Bostic, May 2022, when CPI rose 8.6%

It's a "1-2" Punch?

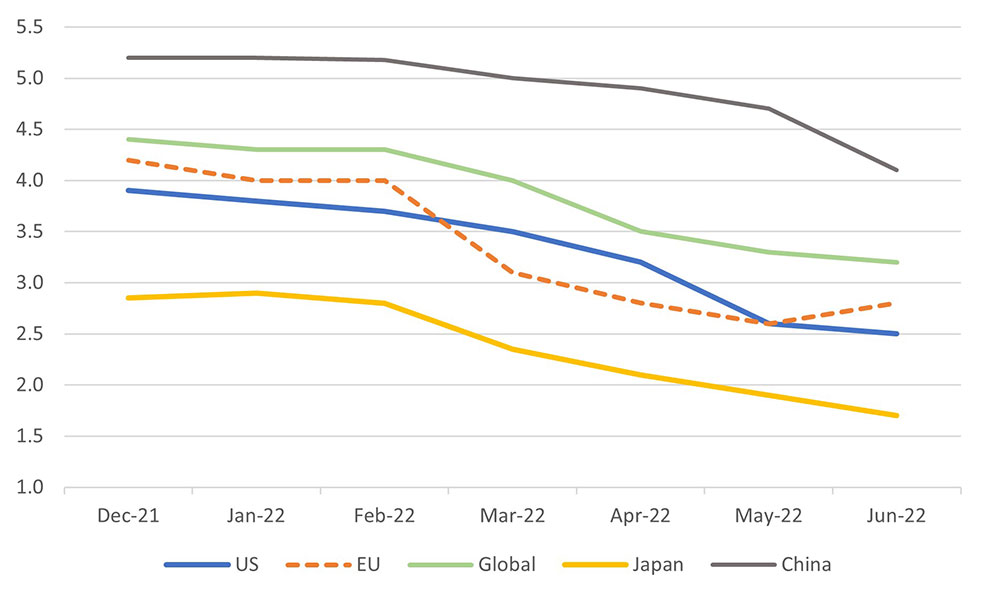

After incipient inflation was missed and the experts were late to the party, the second quarter saw a steady pattern of downgrades to global growth forecasts by most of the major forecast groups including the IMF and World Bank.

Consensus growth forecasts for 2022 have only recently been cut back markedly

Year-on-year %

Source: Bloomberg

Inflation up and growth down. Not a strong backdrop for equity valuations or long duration assets and so the Growth style declined very markedly relative to Value. Value has further to run relative to Growth.

With central bankers increasingly turning hawkish in their monetary policy stance to rein in inflation, the fears of a potential US or global recession have grown recently. Virtually every major central bank has increased interest rates or signalled that they may markedly increase policy rates in the coming months. The futures market has gone from implying a year-end Fed funds rate of 0.8% at the start of the year to building in a US policy rate of 3.3% currently.

If "easy money" is over, what's next? Surely not smaller Government and a return to free enterprise?

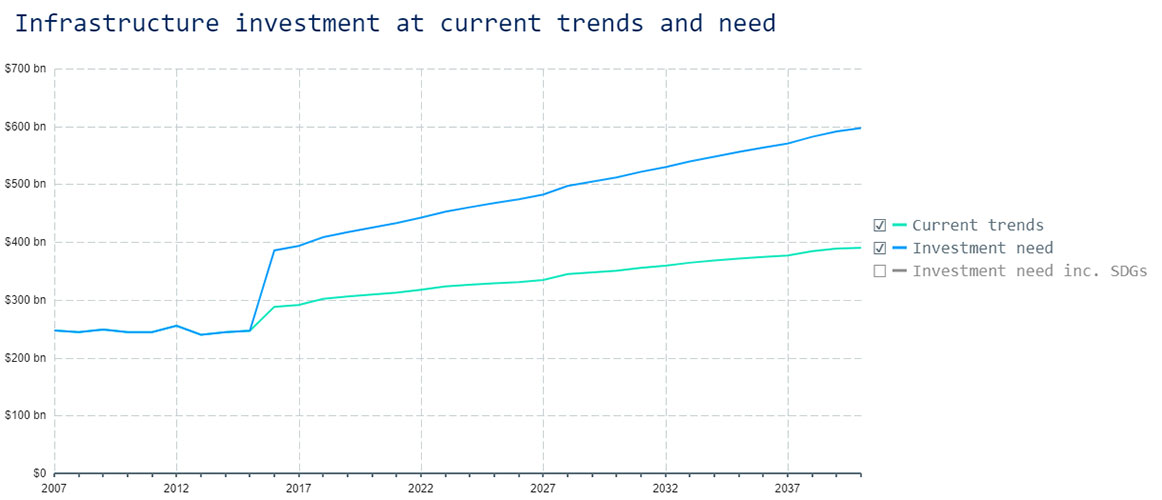

No chance - not (yet?) in the Zeitgeist. It is our assumption that policy makers will not let go of their desire to micro-manage the economy and will now attempt a fiscally based re-set having seen the experiment of free money fail to produce anything like sustainable economic growth. It's not like fiscal spending would be wasted if targeted or incentivised properly although relying on governments to do it efficiently might be naive? We can think of multiple good causes and the multiplier effects on jobs, wages, and productivity would be far more beneficial than a continuation of 'monetary policy for rich people'? Anyone mention Infrastructure, especially in the USA? The chart below is taken from the G20 initiative on Infrastructure and is the estimated shortfall in US total infrastructure spending over the next 40 years based on current trends. Worth a look at the research?

Source: G20 Infrastructure Hub

Should I capitulate?

No but change your investment parameters. Focus on companies that meet 'needs' and not 'wants'. https://www.delftpartners.com/news/views/favour_needs_not_wants.html Favour sensible balance sheets and companies whose cash flows and debt profile will not necessitate returning to markets for increasingly expensive if available at all, financing. Fallen Angels will not be resurrected. Pets.com never did come back; nor did Enron; nor did CMGI. It's over today for many companies like this that were only conceived, born, and nurtured for a while because of euphoria, mania, momentum, infinite amounts of risk tolerance and FOMO. We think that era is over. We hope for a more investment driven backdrop.

So, what should I worry about NOW?

We believe you should manage your asset mix for the following risks or trends:-

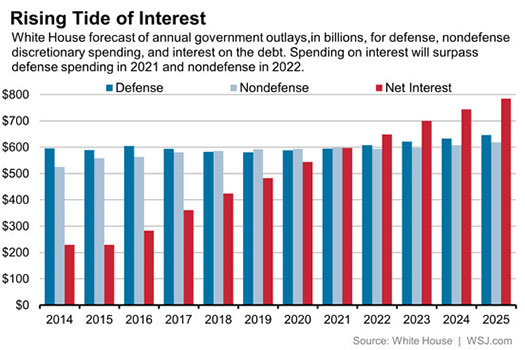

Debasement/Inflation - Invest in inflation hedges such as infrastructure stocks and currencies of countries with a strong Net Foreign Asset position. While money is getting tighter, the chances of cash rates going above inflation as they did in the 1980s, are minimal. Zero probably. There is too much debt. By way of illustration, the US interest bill will almost certainly go from $600bn pa to about $800bn as a result of the repricing of short-term rates. To put that in context the US education and defence budgets are about $700bn each. Therefore, rates which drive debt service costs are unlikely to be allowed to go higher.

Debt - It can't be paid back. Not in the sense of today's values anyway. There will be defaults. Favour companies and countries that have decent balance sheets. Look at net debt not gross; look at debt maturity; beware of bank bail ins (Europe most likely) https://thebusinessprofessor.com/en_US/banking-lending-credit-industry/bail-in-finance-definition Many countries have just passed legislation explicitly allowing for this. The chances of centrally directed capital allocation aka capital controls are not nil, especially in Europe.

Demographics - this matters less as a headwind in reality than it will to sentiment. We believe automation and longer working lives will compensate for lower levels of fecundity and aging demographic profiles. Wage rises are needed relative to profits and this should prompt investment in machine tool companies such as Amada - The "A" in QUAKE https://www.delftpartners.com/news/views/faangs-for-the-memories-but-its-time-to-quake.html

Deglobalisation - the World will not disassemble but a "Plan B" for alternative sourcing and delivery will be on the agenda of every board paper; or should be. Presidents Trump and Biden have both invoked the Defense Procurement Act of 1950 to onshore production of goods deemed necessary. Domestic investment in the West needs to rise. Transport stocks, warehouse companies and smaller companies will benefit. As should working populations in the West since higher investment will lead to more jobs, higher pay. Buy backs running at almost $1 tln in the USA only really benefit the C suite. There are better uses for this money and we hope but don't expect tax incentives to rebalance company decisions to favour investing over buy backs.

Decarbonisation - We cannot possibly do justice to this (ahem) debate here but regardless of what Steve Koonin thinks of the science (https://www.wsj.com/articles/unsettled-review-theconsensus-on-climate-11619383653) or Professor Michael Kelly thinks of the cost benefit (https://wattsupwiththat.com/2022/03/06/michael-kelly-exposes-the-implications-of-net-zero/), it's a project with immense political appeal and so is with us. Our suggestion is that we will now see a much better managed and planned transition to so called Green energy which means…MORE investment in Gas and Oil to bridge the switch. There is already some demand destruction of these commodities, but they are not going back down much. Given the choice, would you rather Germany recommissioned 4 lignite powered electricity stations, or invested in a series of LNG pipelines and off take facilities to import and distribute US LNG? It's already done the former because it has had to, given a poorly designed Green transition, but was actually warned to do the latter about 5 years ago by everyone's favourite global leader - just saying. We know what they should have done. They still might?

Concluding, we think we're at a crossroads.

The free money experiment is over, and the likelihood is that policy makers insist on imposing a different paradigm but this time with a fiscal dimension. It will be done with your money. A return to more 'laissez-faire' would be better for all eventually but would be more painful in the short term.

We can either have much higher rates, with a crushing recession to squeeze inflation, and inflation expectations, and a gradual loosening of regulation and a reduction in subsidies (laissez-faire) OR…

a bit of inflation accompanied by a switch to a government directed fiscal push.

Given a choice between killing inflation with an interest rate increase and letting markets decide the clearing price of debt and equities, that near term will cause an asset price crash, and higher unemployment, OR imposing a gentle bit of monetary restraint accompanied by rhetoric about how inflation is temporary and "a price worth paying and it's Putin to blame anyway", they will 100% go for the latter. Short term pain is never a popular choice for politicians.

Our advice is Value equities, a bias to smaller companies, and "useful" real assets, (eg roads, bridges hospitals, schools, logistics warehouses all available via REITs) and, currently at least, short duration quality bonds. We believe that prices of energy and other industrial inputs, consumer goods, and of course wages, will remain elevated at these new levels since supply side takes time to gear up, but the rate of change of prices - inflation - will be soon peaking due to year-on-year comparisons. This will help sentiment toward risk assets. Consequently, dividend paying equities geared to the fiscally based re-set, especially if they fall into 'on sale" territory, are our favourite. We have tried to capture this in all our strategies.

Delft Partners July 2022

DISCLAIMER

This report provides general information only and does not take into account the investment objectives, financial circumstances or needs of any person. To the maximum extent permitted by law, Delft Partners Pty Ltd, its directors and employees accept no liability for any loss or damage incurred as a result of any action taken or not taken on the basis of the information contained in the report or any omissions or errors within it. It is advisable that you obtain professional independent financial, legal and taxation advice before making any financial investment decision. Delft Partners Pty Ltd does not guarantee the repayment of capital, the payment of income, or the performance of its investments. Delft Partners operates as owner of API Capital Advisory Pty Ltd AFSL 329133.