Taiwan: Not the Most Dangerous Place on Earth

May 2021

By Delft Partners

As long-term investors in Taiwan we prefer to look at the investment flows by Taiwanese companies into China as an indicator of the state of relations and not media speculation regarding the prospect for military hostilities. If China were going to invade Taiwan it would have happened years ago. The financial relationship between China and Taiwan is strong and growing. It is that financial relationship which will ultimately guide China and Taiwan to a sensible compromise regarding political differences.

Taiwan has been in the news a lot recently, especially with media headlines highlighting the apparent threat of invasion by China. In Australia we have seen this being used as a justification for increased military budgets in part to support the defence of Taiwan. We have been investing in the market in Taiwan since it opened to international investors in the early 1990s. Taiwan has some world class companies and was recently awarded four of the top one hundred places in the survey of global innovation published by Clarivate, not bad for a small island population of 23.5m people. We expect to continue to invest in world class companies that are headquartered in Taiwan and prefer to focus on the flow of investment money that takes place between Taiwan and China rather than speculation about imminent invasion.

April was a month of very mixed performance in the Asian region, by far the strongest market was Taiwan where the small to mid-sized stocks increased by 13.1% bringing the return over one year +75.8%. The broader measure of market performance in Taiwan for large capitalisation stocks increased by 7.7% during the month of April and +82.3% over one year. This was despite “The Economist” announcing Taiwan as the most dangerous place on Earth. “The Economist” was highlighting risks of military action by China to seize control of Taiwan. While China has been increasing incursions into Taiwan’s airspace, their way of testing responses, this is not anything new, China has a long history of this behaviour and we do not see this as the move towards an invasion of Taiwan.

In recent months we have seen China objecting to the United States Navy movements through the Taiwan Straits. In February there was tension between China and the United States when the destroyer USS Curtis Wilbur sailed through the Taiwan Strait, with China suggesting that the United States was undermining regional peace and stability. The United States sends their Navy vessels through the Taiwan Strait on a regular basis in a show of support for Taiwan, this however is a token show of support. The official United States policy of formal defence of Taiwan ended in 1979 when it ceased with recognition of the Republic of China as “China” and started referring to it as “Taiwan”. This change of status occurred when the United States recognised the People’s Republic of China as “China” and all relations with Taiwan then became informal.

Late in 2020 Beijing made an explicit warning that independence for Taiwan “means war”. China’s Taiwan problem dates back to 1949 when the Communist Party seized control of the Mainland and the displaced Kuomintang (KMT) government relocated to Taiwan. China has never renounced the use of force to take control of Taiwan, however, overt verbal threats of conflict are rare. The current ruling party in Taiwan, the DPP previously talked about “independence”, however, that word has been quietly removed from the narrative employed by the party. Relations with China tend to worsen when the DPP hold power and improve when the KMT hold power which is somewhat ironic given that the KMT were the original enemy of the Communist Party during the civil war that concluded in 1949. We can expect better progress towards a form of political accommodation between China and Taiwan the next time the KMT hold office in Taiwan.

A good deal of the recent tension regarding Taiwan can be attributed to the former US Administration under Donald Trump due to increased military equipment sales and US Navy activity through the Taiwan Strait. We expect the Biden Administration to adopt a lighter touch with respect to Taiwan. We have already seen Vice President Wang Qishan indicating to a delegation of US representatives that common interest outweighs differences with the United States. A period of relative stability with respect to trade and an end to the arbitrary Trump imposed tariffs will be taken very positively by markets.

Taiwan’s President Tsai Ing-wen responded to “The Economist” headline assuring everyone that the government is fully capable of managing all potential risks and protecting Taiwan from danger. President Tsai went on the speak about responding prudently to regional developments and overcoming the challenges posed by authoritarian expansion in a reference to China without naming China. The equity market in Taiwan was much more interested in the news that the local economy grew by 8.16% in the first quarter, the fastest growth recorded in a decade and well above consensus expectations. The positive growth surprise was driven by stronger domestic manufacturing and demand for exports. Two of Taiwan’s major semiconductor manufacturers have recently announced large investment programmes aimed at alleviating the worldwide shortage of semiconductors needed in the automotive industry and consumer products. Taiwan is expected to achieve economic growth in excess of 5% for the full year of 2021.

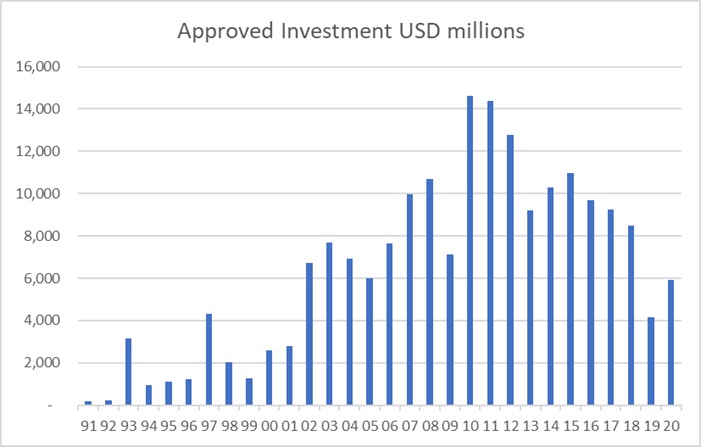

The table shows officially sanctioned investment that have taken place by Taiwanese companies investing in China. From the start of 1991 to the end of 2020 there have been 44,400 investments from Taiwan into China totalling USD 192.4 billion. By way of context, China received a total of USD 141 billion of foreign direct investment in 2019. Typically, “Hong Kong” appears as a major contributor to investment in China and this is usually money from Taiwan that has to be channelled via entities in Hong Kong. China’s official policy position is that Taiwan is a domestic province of China and therefore investment flows sourced from Taiwan should not be treated a foreign source of investment.

While the annual flow of aggregate investment funds from Taiwan to China have slowed from the USD 14 billion annual peaks in 2010 and 2011, the figure in 2020 approached USD 6 billion and remains a substantial number. It is also important to note that the 2020 level showed a substantial uplift from the 2019 number which was a response to the then President Trump’s habit of surprise tariff restrictions being applied to China. For a while China was the predominant area of manufacturing investment by Taiwanese companies, the cost savings from manufacturing in China were too tempting to resist. The rising cost of labour in China and then Trump’s trade war prompted a sensible diversification of investments by the Taiwanese to ensure that China did not end up putting their supply chain at risk. The cost savings of manufacturing in China available a decade ago are much less pronounced in the current environment.

An example from our portfolio in Taiwan is Novatek Microelectronics, a leading fabless chip design company specializing in the design and development of a wide range of display driver integrated circuits required for sophisticated flat panel displays and audio/video applications for all digital devices. We originally acquired our position in Novatek at an average price of TWD 102 in late 2018, those shares recently reached the TWD 600 level. We have taken profits along the journey and remain a happy shareholder in a business that is attractively valued especially versus global peers. We acquired the position on a p/e ratio of 11x, since then profits have expanded from TWD 6 billion in 2018 to more than TWD 20 billion in the current year, putting the company on 14x p/e and a net yield in excess of 4%. Novatek has eight of their eleven global sales offices located in China, their relationship with China remains crucial to the prospects of the business. Novatek opened their first office in China ten years ago. Going forward, the company expects to achieve significant growth in Japan and South Korea in addition to ongoing development of sales in China. Novatek typically invests the equivalent of 14% of revenues on R&D, a significant and ongoing commitment to the intellectual capital of the business. In the field of display driver integrated circuits, Novatek has global market share of 20%, second only to Samsung at 30%.

In conclusion, as long-term investors in Taiwan we prefer to look at the investment flows by Taiwanese companies into China as an indicator of the state of relations and not media speculation regarding the prospect for military hostilities. If China were going to invade Taiwan it would have happened years ago. The financial relationship between China and Taiwan is strong and growing. It is that financial relationship which will ultimately guide China and Taiwan to a sensible compromise regarding political differences.

Insights by Australian Fund Monitors Pty Ltd (AFM) provides investors and advisors with commentary and articles originated and provided by fund managers and other contributors. The views and opinions contained within each Insights article are those of the contributor and do not necessarily reflect those of AFM. www.fundmonitors.com.

DISCLAIMER

Australian Fund Monitors Pty Ltd, holds AFS Licence number 324476. The information contained herein is general in its nature only and does not and cannot take into account an investor's financial position or requirements. Investors should therefore seek appropriate advice prior to making any decisions to invest in any product contained herein. Australian Fund Monitors Pty Ltd is not, and will not be held responsible for investment decisions made by investors, and is not responsible for the performance of any investment made by any investor, notwithstanding that it may be providing information and or monitoring services to that investor. This information is collated from a variety of sources and we cannot be held responsible for any errors or omissions. Australian Fund Monitors Pty Ltd, A.C.N. 122 226 724